Join Our Telegram Channel

Join Our Whatsapp Group

Waec Financial Accounting 2024 Answers, waec Accounting answers 2024, Waec Accounting 2024 question, Waec 2024 Financial Accounting essay and obj Answers, Financial Accounting waec 2024, Here is the only legitimate website where can get the 100% Verified Waec 2024 Acounting Answers. and also have the chance to score A's , B's and C's in this ongoing Waec 2024 Financial Accounting Examination. We Assure you of getting the waec Financial Accounting questions and answers 2024 on time, only those that subscribed. WE DONT SCAM, ONLY A TRIAL WILL CONVINCE YOU

Tuesday, 21st May 2024

Financial Accounting 2 (Essay) 9:30 – 12:00pm

Financial Accounting 1 (Objective) 12:00pm – 1:00pm

FIN. ACCOUNTING OBJ:

1-10: CDBACACBBC

11-20: CDDBDBDACB

21-30: AADCCBBBBB

31-40: ACBBDDADAA

41-50: CCDABDBBCD

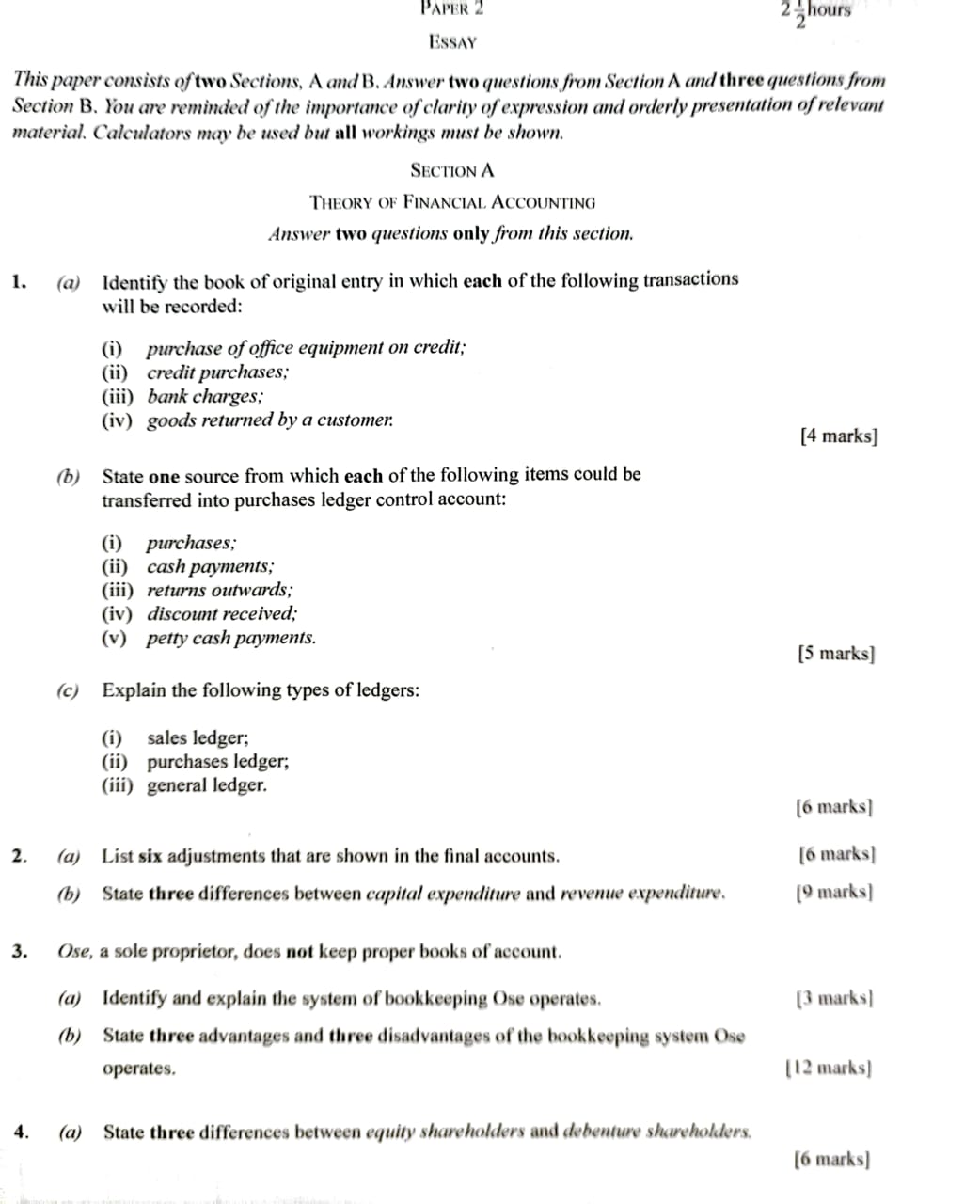

PLEASE NOTE: YOU’RE TO ANSWER TWO(2) QUESTIONS ONLY FROM SECTION A

AND THREE(3) QUESTIONS ONLY FROM SECTION B

(1a)

(i) Purchase of office equipment on credit: General Journal

(ii) Credit purchases: Purchases Day Book

(iii) Bank charges: Cash Book

(iv) Goods returned by a customer: Returns Inwards Book

(1b)

(i) Purchases Journal: The total of all credit purchases is transferred from the purchases journal.

(ii) Cash payments: Details of payments made to suppliers are recorded in the cash book.

(iii) Returns outwards: This journal records goods returned to suppliers.

(iv) Discount received: Discounts received from suppliers are recorded in the cash book along with payment details.

(v) Petty cash payments: Small payments made through petty cash are recorded in this book.

(1c)

(i) Sales Ledger: The sales ledger contains individual accounts for each customer. It tracks all sales made on credit, payments received from customers, and any returns or allowances. This ledger helps in monitoring outstanding receivables and managing customer accounts.

(ii) Purchases Ledger: The purchases ledger includes individual accounts for each supplier. It records all credit purchases from suppliers, payments made to suppliers, and returns outwards. This ledger assists in managing outstanding payables and supplier accounts.

(iii) General Ledger: The general ledger is the central repository of all financial transactions in a business. It contains all the accounts necessary to prepare financial statements, including assets, liabilities, equity, revenues, and expenses. Each transaction recorded in the books of original entry is posted to the relevant accounts in the general ledger. This ledger provides a comprehensive overview of the company’s financial position and performance.

(2a)

(PICK ANY SIX)

(i) Accrued Expenses

(ii) Prepaid Expenses

(iii) Accrued Income

(iv) Unearned Income (Deferred Income)

(v) Depreciation

(vi) Bad Debts

(vii) Provision for Doubtful Debts

(viii) Inventory Adjustments

(ix) Amortization

(2b)

(PICK ANY THREE)

(i) Capital Expenditure is incurred to acquire or improve long-term assets, such as property, plant, and equipment whereas Revenue Expenditure is Incurred for the day-to-day running of the business and to maintain the existing assets.

(ii) Capital Expenditure provides benefits over a long period, usually more than one accounting period while Revenue Expenditure provides benefits within the current accounting period.

(iii) Capital Expenditure is recorded as an asset in the balance sheet and depreciated over its useful life while Revenue Expenditure is Charged directly to the income statement as an expense in the period it is incurred.

(iv) Capital Expenditure affects both the balance sheet (increase in assets) and the income statement (depreciation expense) while Revenue Expenditure directly affects the income statement by reducing profit for the period.

(v) Capital Expenditure costs are capitalized, meaning they are added to the value of the asset and amortized over time while Revenue Expenditure costs are expensed in the period they are incurred and do not appear on the balance sheet.

(3a)

Ose operate with Single Entry System of bookeeping. This system is typically used by small businesses or sole proprietors who do not keep proper books of account. In the single entry system, only one side of each transaction (either debit or credit) is recorded, which contrasts with the double entry system where every transaction affects at least two accounts.

(3b)

ADVANTAGES:

(PICK ANY THREE)

(i)The single entry system is easy to understand and use, making it accessible to those without formal accounting knowledge. It involves fewer records and less complex procedures.

(ii)Implementing and maintaining a single entry system is inexpensive. It does not require advanced accounting software or professional accountants, which can be costly for small businesses.

(iii)This system takes less time to manage compared to the double entry system. Business owners can spend more time focusing on their core operations rather than on detailed bookkeeping.

(iv)The single entry system requires minimal paperwork and fewer records. This reduces the administrative burden on the business owner.

(v)The system offers flexibility as it does not follow strict accounting rules and procedures. This can be advantageous for small businesses with straightforward transactions.

DISADVANTAGES:

(PICK ANY THREE)

(i)The single entry system can lead to incomplete and inaccurate financial records. Since it does not track both sides of transactions, there is a higher risk of errors and omissions

(ii)Due to the lack of checks and balances inherent in the double entry system, the single entry system is more susceptible to fraud and errors. It is difficult to detect discrepancies and irregularities.

(iii)The limited financial information provided by the single entry system makes it difficult for business owners to make informed decisions. Critical financial metrics and insights are often missing.

(iv)Financial institutions typically require detailed and accurate financial records when assessing loan applications. The single entry system’s lack of comprehensive financial data can make it difficult for businesses to obtain financing or attract investors.

(4a)

(PICK ANY THREE)

(i)Equity Shareholders are owners of the company and hold a share of the company’s residual assets. While Debenture Shareholders are creditors to the company and do not have ownership rights; they hold a company’s debt instruments.

(ii)Equity Shareholders generally have voting rights, allowing them to influence corporate decisions and elect the board of directors. While Debenture Shareholders do not have voting rights and cannot participate in corporate governance

(iii)Equity Shareholders earn dividends, which are not guaranteed and depend on the company’s profits. While

Debenture shares earn fixed interest payments, which are guaranteed and must be paid regardless of the company’s profitability.

(iv)Equity Shareholders have the last claim on the company’s assets in the event of liquidation, after all debts and other liabilities have been settled. Whole Debenture Shareholders have a higher claim on the company’s assets than equity shareholders and are paid before them in case of liquidation.

(v)Equity Shareholders bear higher risk due to variability in dividends and no guaranteed return, but they have the potential for higher rewards through capital gains. While Debenture Shareholders bear lower risk as they receive fixed interest payments and have a guaranteed return, but they do not benefit from capital gains as equity shareholders do.

(4bi)

Cumulative Preference Shares: Cumulative preference shares accumulate unpaid dividends. If a company is unable to pay dividends in a given year, the unpaid dividends are carried forward to future years. These must be paid out before any dividends can be given to equity shareholders in subsequent years.

(4bii)

Redeemable Preference Shares: Redeemable preference shares can be bought back (redeemed) by the issuing company after a certain period or on a specified date at a predetermined price. This provides the company with flexibility in managing its capital structure and allows shareholders to know when they can expect their capital to be returned.

(4biii)

Participating Preference Shares: Participating preference shares entitle shareholders to a fixed dividend and an additional dividend based on certain conditions, usually related to the company’s profitability. They also may receive a portion of the residual assets upon liquidation after all debts and fixed dividends have been paid.This provides an opportunity for higher returns in profitable years.

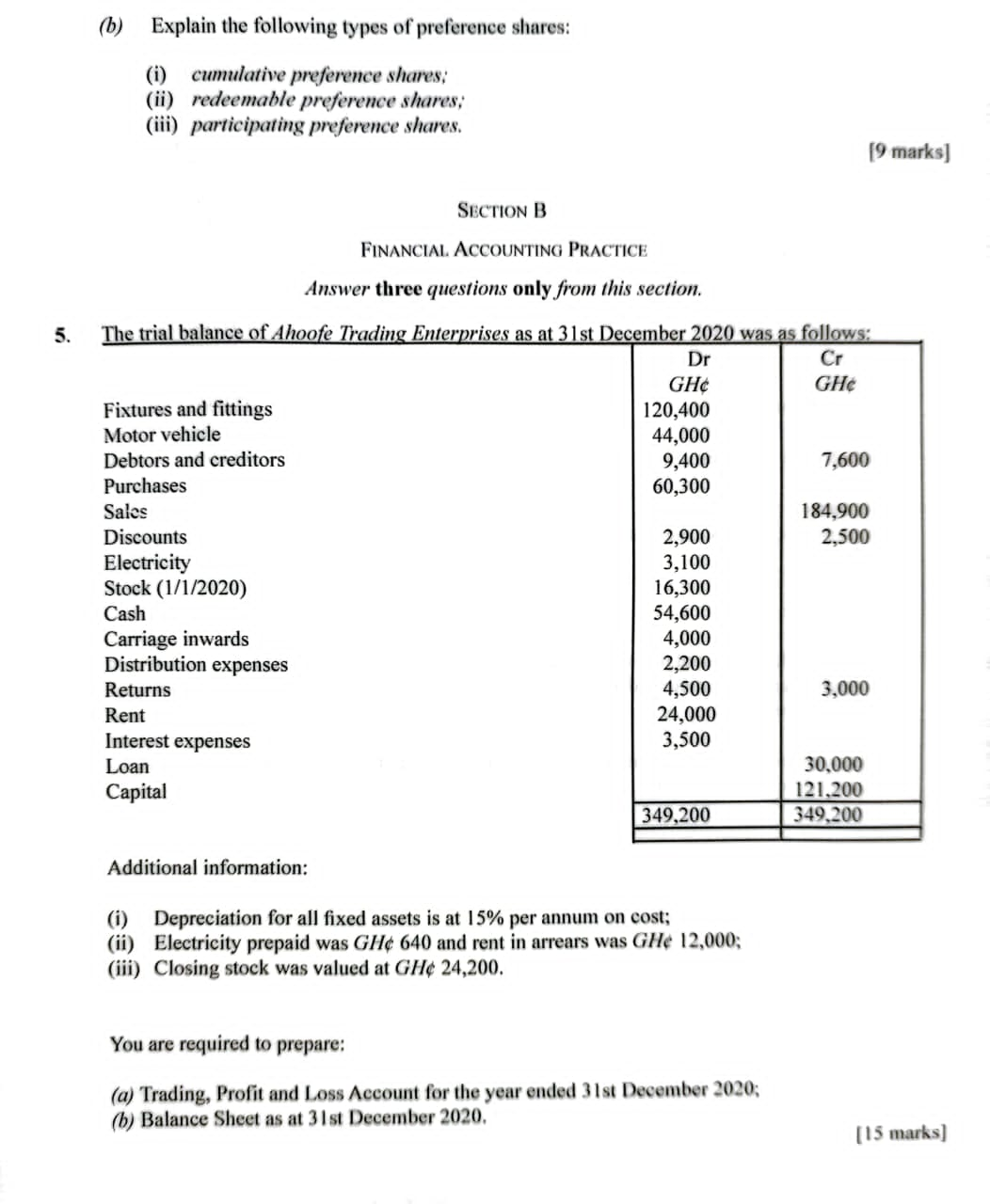

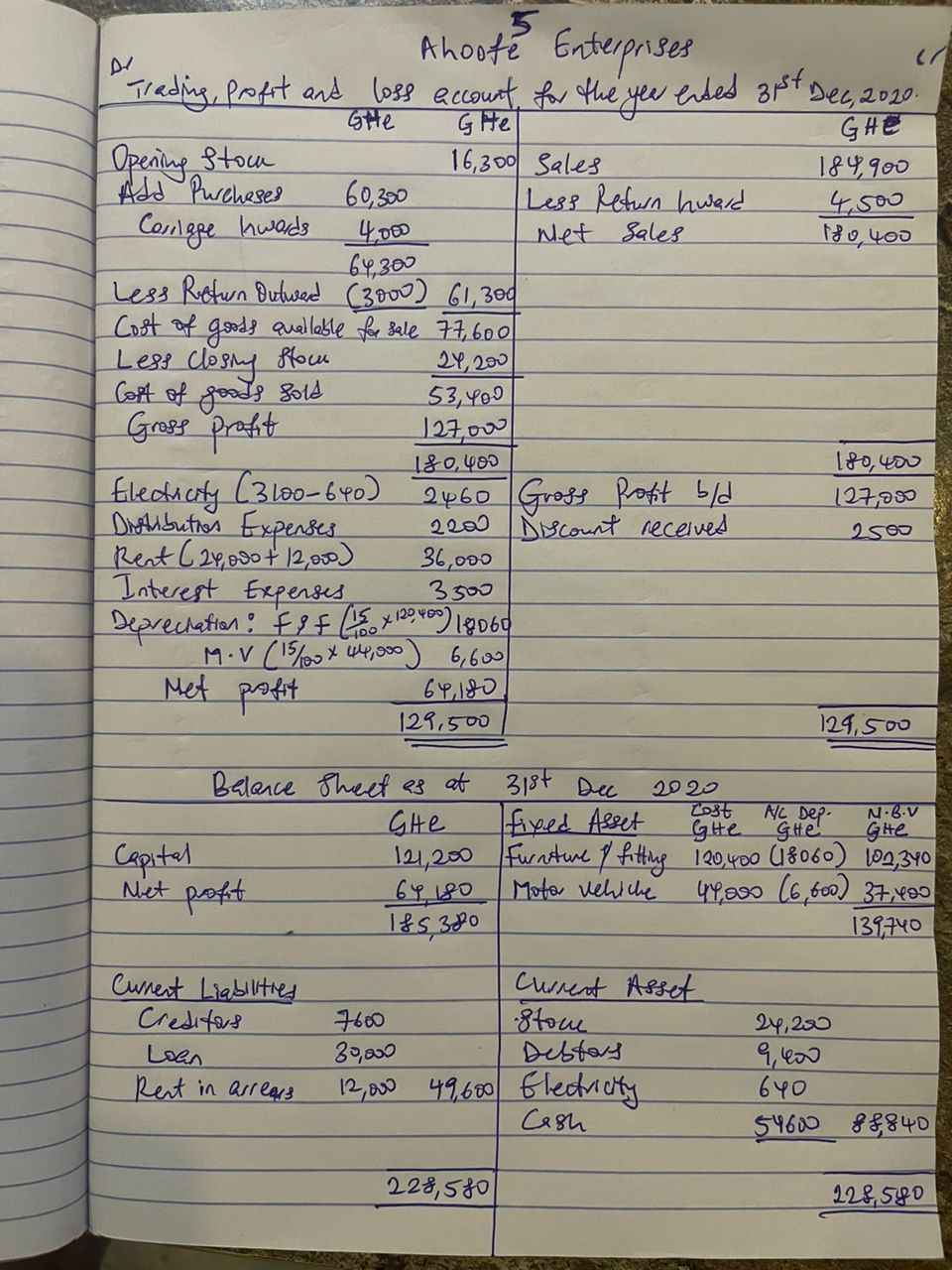

(5)

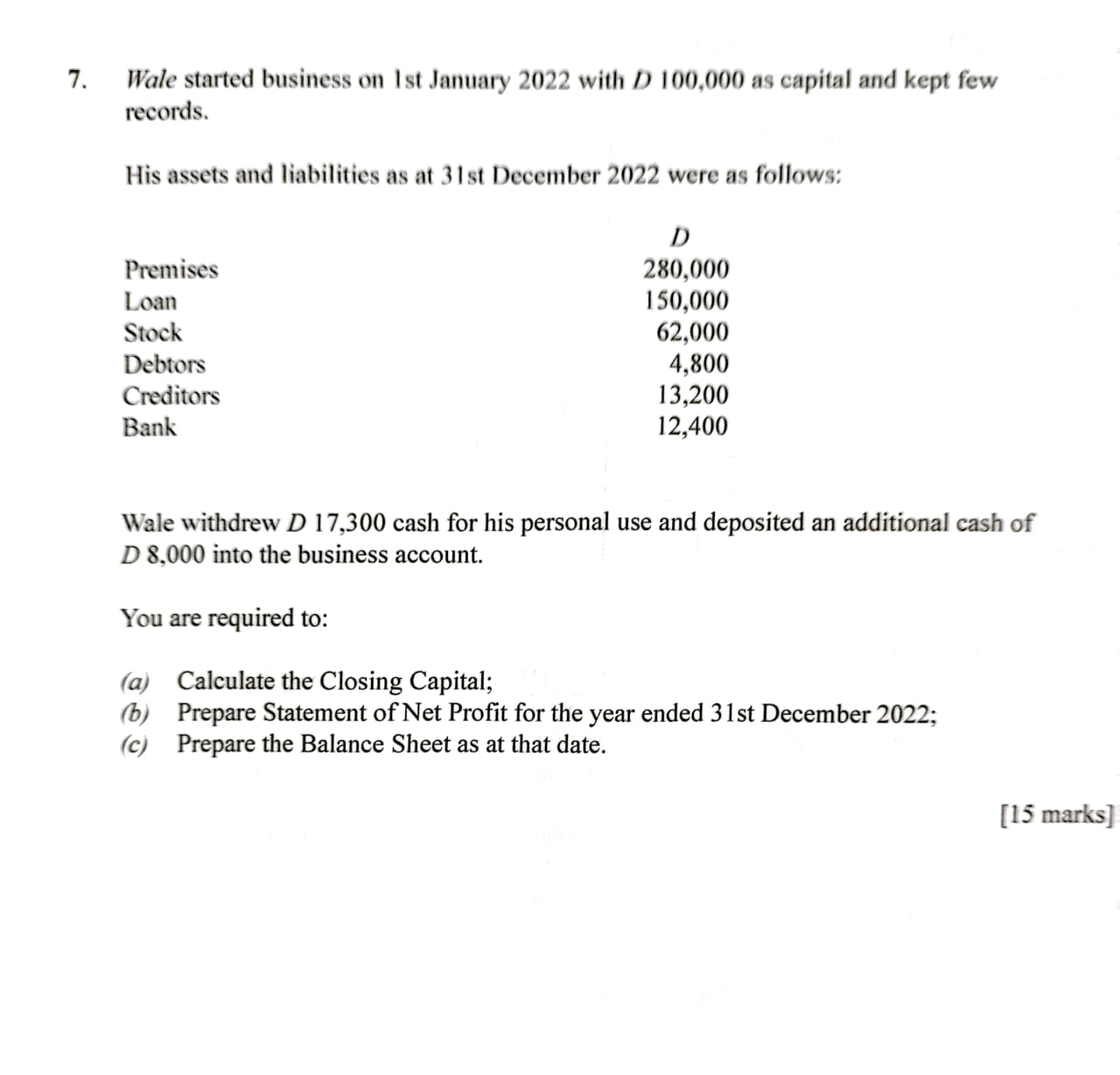

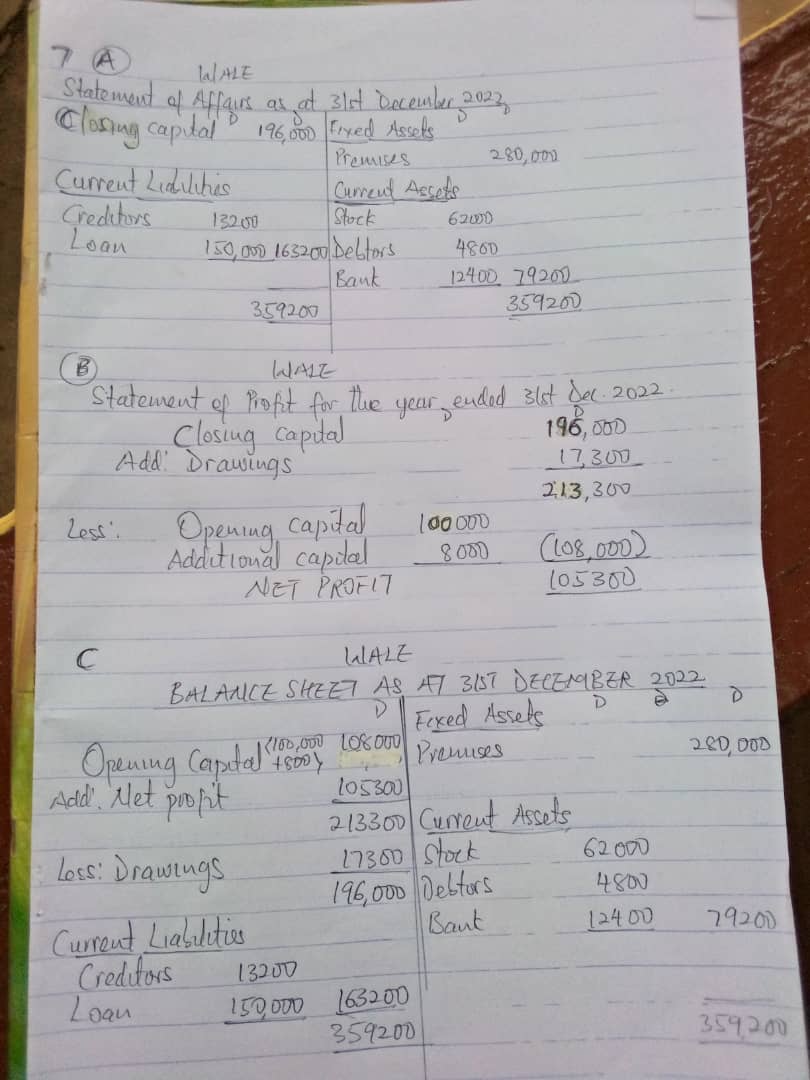

(7)

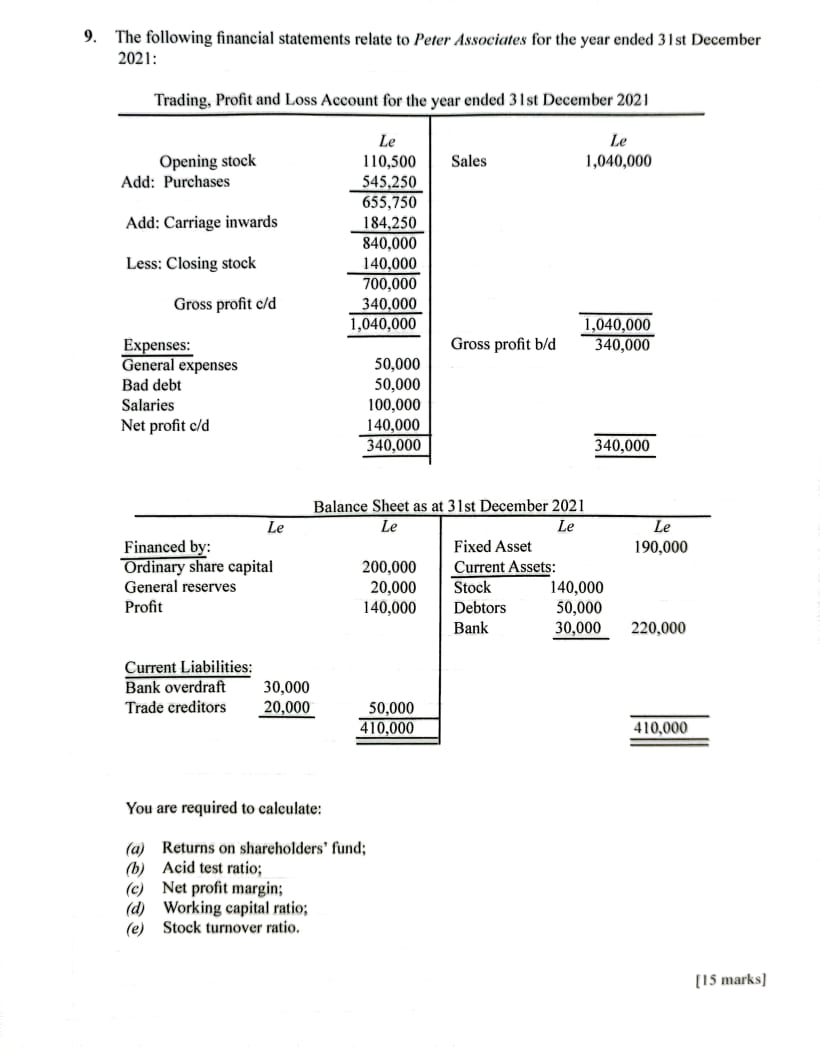

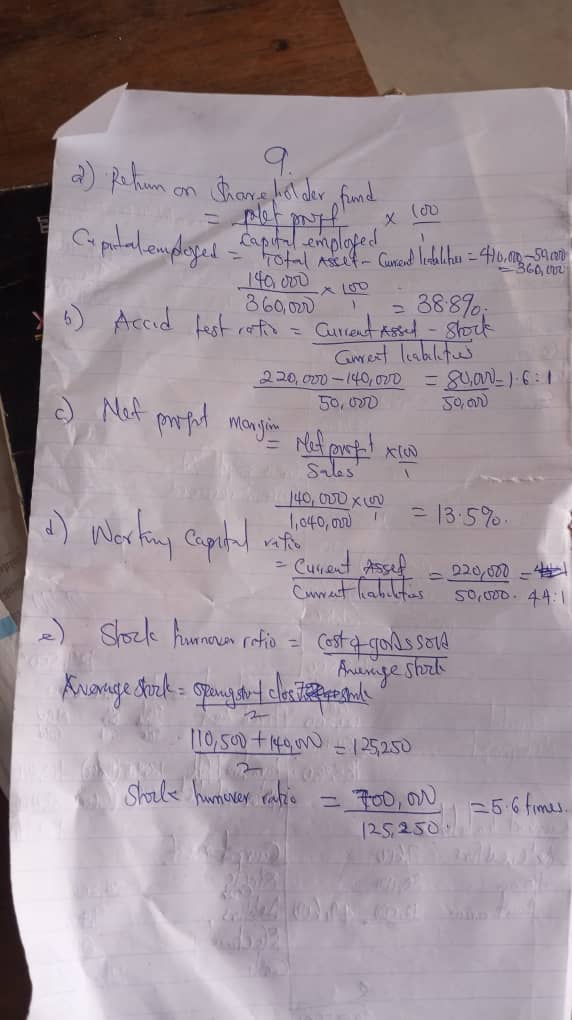

(9)

Answers Loading...